Look at all your expenses. Start with what can't be changed - your rent / mortgage, debt payments, student loans, childcare costs, etc. Write down all your fixed expenses and tally them up. How much do you have left to work with?

Now look at semi-fixed expenses - utilities may vary a bit, but are they generally about the same each month? Phone, internet, cable, insurance - things that could be lowered just a bit. Can you get on a steady payment plan with your electric company where you pay an average (fixed) amount each month? Can your cell phone plan be changed to lower your bill? Do you really watch all those channels, or can you reduce your cable package? When was the last time you checked your insurance rates? Simply making a few phone calls or checking around online can reduce these expenses quite a bit.

Now comes the harder expenses. First, we will look at monthly variable expenses, then we'll explore those not-so-regular expenses, like gifts, that still come up, just not every month.

Monthly expenses. Food is often the biggest surprise when starting a budget. It's easy to spend more than expected at the grocery store, go out to eat a little more than planned, make those unexpected trips to the market and end up with a few extra things. Really analyze how much you spend in this category. Can you reduce how often you eat out? Can you buy less convenience foods? Could you plan out your meals better and buy only what you need? There are countless ways to save on groceries, from sales to coupons to meal planning. Set a reasonable goal and try to reduce it a bit each week. If you try to drastically change it all at once, you will surely fail. Start by trimming down $50 or even $25 each week and work your way up. Consider your schedule when doing this. If you know you have back to back soccer games on Saturdays or you always eat with the family after church, include that in your budget and planning. Food may be one of the most challenging areas, but it's also one of the easiest places to shave off a few dollars.

Other monthly expenses you could cut back on with little effort are fuel (plan your trips better, carpool, etc), babysitting (reduce how often you go out alone or consider taking the kids with you), entertainment (look for cheaper alternatives, have a movie night at home, check for coupons), and personal hygiene / grooming ( go a week longer between haircuts, try an at-home trim or dye, use coupons for products you buy regularly, make your own products at home). There are countless ways to trim a few dollars here and there, which can make a big difference overall.

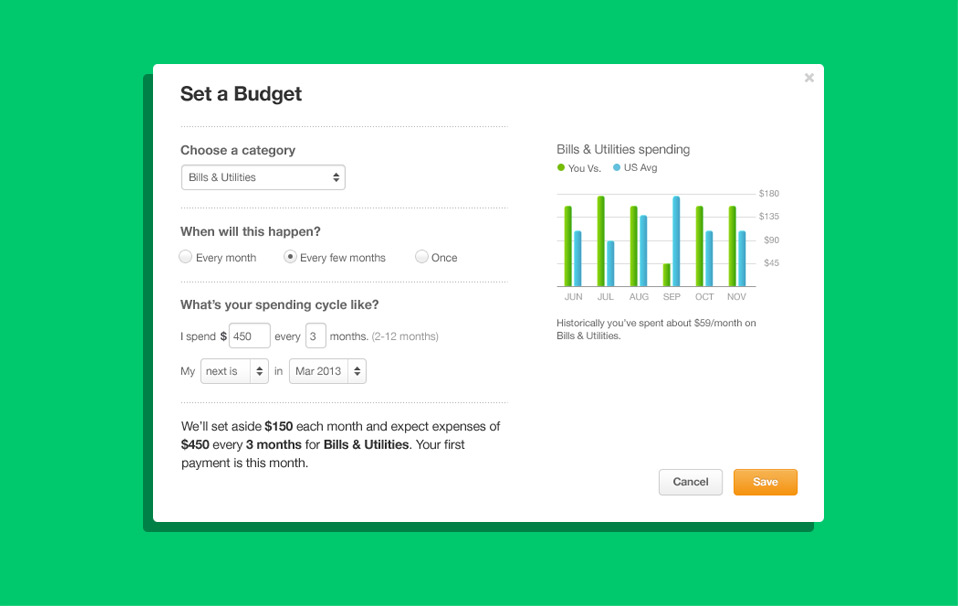

Now for those irregular but inevitable expenses. Consider how much you spend at Christmas time (and how broke you are in January!). What if instead you put aside $25 every month, so when December rolls around you already have the cash. And if you set aside $20 every month for other gifts (and let it roll over each month it's not used), then Mother's Day, Father's Day, Valentine's Day, Easter, Anniversaries, and Birthdays won't be so hard on your budget. Car repairs and maintenance- you know you're going to need it, why not plan for it? If you budgeted for $30 a month for car maintenance, then when you need that new wiper blade, oil change, or brakes, you've already got the cash. The key here is to plan. You know they will eventually happen, even if it's not every month. Look at your expense list again, and pick out all the irregular expenses (clothing, gifts, repairs, home maintenance, school supplies, club dues, sporting equipment and fees, etc). You can combine some or keep them all separate and give them a line in the budget each month.

If you set up a Mint account in Part 1, it will help you with this part. You can create a budget category for every expense, and it gives you the option to rollover any unused portion - like for gifts and maintenance. Then you can easily see at any time how much you've spent in each category.

Go line by line and see if you can reduce each expense, even if it is only by a few dollars. Remember, every little bit helps and they can add up to a big difference. Make sure every expense you listed has a place in the budget, and make sure it is realistic for your family. If you've been spending $300 a month eating out, cutting it out completely won't work. Reduce it to $150, then when you are comfortable with that, cut back a little more. Every budget is a work in process and it's okay to tweak it each month. Be sure to include savings in your budget - both long and short term (eg: retirement and emergency fund), so life's little mishaps don't catch you off guard.

In Part 3 we will go over how to stick to the budget. Right now, just focus on creating a budget that works for you. No two budgets will be alike, you have to figure out what works best for your family. If you have athletic children, you'll probably spend more on sports equipment. If you are an artsy family, craft supplies may be a larger expense. The main points to remember are to account for every expense, and reduce everything you can.

No comments:

Post a Comment